A look at the day ahead in European and global markets from Wayne Cole.

A muted start to the week in Asia with Chinese data too mixed to provide much momentum as political uncertainty in Europe lurks in the background….

It was notable that no less than five European Central Bank sources stressed to Reuters that the institution was not planning any emergency buying of French bonds, knowing the market will be pushing for exactly that.…

In a politically driven market (French electio) a key is to identify when the market is trading on this upcoming event and when it is in the background.

This chart is clear —

Key levels are at the 1.0667 low (major levels 1.0649 and 1.0600) and 1.0745 (suggests limited upside unless 1.0750 trades, stronger bias if it stays below 1.0719

A run of Chinese monthly data open the week on Monday amid expectations for steady, unspectacular results. But it will be central bank announcements that will be the week’s key focus beginning with the Reserve Bank of Australia on Tuesday followed on Thursday by China’s loan prime rates then the Swiss National Bank and finally the Bank of England. No rate changes are expected with the exception of the SNB where forecasts range from no change to rate cuts of either 12.5 or 25 basis points. Note that Wednesday’s consumer price report from the UK could have a bearing on future expectations for BoE action with moderation to a benign 2.1 percent Econoday’s CPI consensus.

Retail sales on Tuesday will be the most watched US report; forecasters are looking for no more than modest gains across key readings. Japanese data will open with machinery orders on Monday, merchandise trade on Tuesday, and will be capped by May consumer prices on Friday where higher costs for renewable energy are expected to heat up the headline print. The week will close with Friday’s run of June PMI flashes where incremental improvement is the general consensus.

Kashkari said (Sunday the 16th)

–

* it’s ‘reasonable’ to predict December rate cut

* Fed Well-Placed to Take Its Time Ahead of Rate Cut

* “We need to see more evidence to convince us that inflation is well on our way back down to 2 percent. The good news is as you’re reporting this indicator, the job market remains strong,”

Polls put left-wing ‘Popular Front’ coalition in second

BORGO EGNAZIA, June 14, Italy (Reuters) – France is facing a “very serious” moment as parliamentary elections loom, said President Emmanuel Macron on Friday, with financial markets rattled by the country’s far-right and far-left political blocs currently leading polls.

Polls put left-wing ‘Popular Front’ coalition in second

BORGO EGNAZIA, June 14, Italy (Reuters) – France is facing a “very serious” moment as parliamentary elections loom, said President Emmanuel Macron on Friday, with financial markets rattled by the country’s far-right and far-left political blocs currently leading polls.

The FED keeps on yakking about CUT. Cut(s) is/are coming.

The economy is at “full employment” & financial markets are at 10,000 degrees F. Their dots are supposed tell THE market what they are expecting (hahaha bamboozle) , Jerome likes to hear himself talk about being flexible (i.e. by allegedly custom-fitting response to incoming data IF this comes in then that blablah)

With reference to the 10-yr yield:

As a degenerate trader focused on using the FED (and the Treasury) for juicing profits from their policies and the simple reality that the FED is buying Treasury Bonds (thereby allowing congress to spend n spend) I am working on this assumption:

While 10-yr yield is under 4.5% the FED is

1) in the market buying Treasuries

2) suppressing yield and

3) screaming at Congress: “spend. SPEND!”

and so their supposed quest at quenching inflation is not serious.

For me any incoming data that would suggest a turn in “higher for longer” or even an imminent cut is smoke while 10-yr yield is below 4.5%

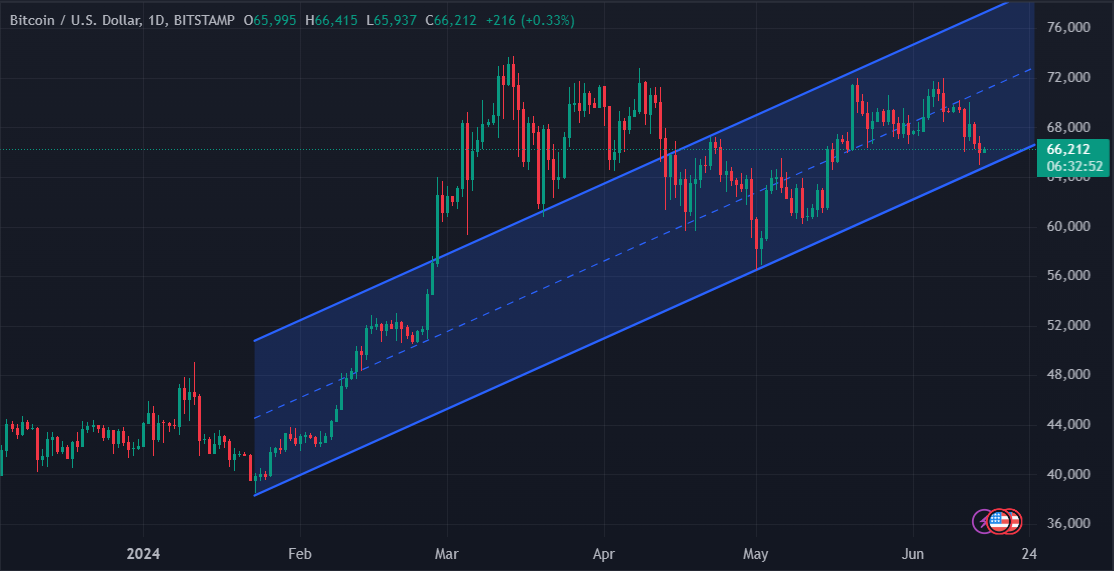

Bitcoin crashes below $66K, More pain ahead?

Bitcoin dropped more than 2% in the last 24 hours to drop the $65,000 price level during the US trading session straight down from around $67,000. Over the past seven days, BTC has declined by 7.5%, marking its weakest price in four weeks.

S&P 500 Posts Weekly Gain, Closes Near Record Highs as Technology Sector Rallies

The Standard & Poor’s 500 index rose 1.6% this week, reaching new highs, led by the technology sector.

The market benchmark closed Friday’s session at 5,431.60, slightly below its record closing level of 5,433.74 reached on Thursday. The S&P 500 also hit a new intraday high on Wednesday at 5,447.25. It is now up 2.9% for the month to date and up 14% this year.

As a trader, all you should want from a broker is one that is repotable, provides you with a level playing field, and one you don’t have to worry about being in business when you wake up.

This past week started out with the EURO coming under selling pressure on French political concerns, got a reprieve mid-week when US CPI came in soft, and ended it on a weaker note with French politics again the focus. However, it did manage to come off its lows after EURUSD paused above its 2024 low.

This sets the stage for the coming week where a light US calendar leaving the focus elsewhere.