Before it breaks on either side, and taking into account geopolitical situation right now I am going to stay away from trying to call some larger moves.

Going solely Intraday – right now trying for higher, but need a signal to confirm.

The week is starting out with some relief that geopolitical risks have not escalated further. It is like trying to pick up the pieces after a hurricane or tsunami hits your town.

This leaves EURUSD consolidating where 1.0650 seems to be pivotal with no key nearby resistance.

Risk is still pointed down but would need to take out 1.0622 to build further momentum.

Given the one-way move down, use FIBO levels to give some order to the price action using our

No better-than-mixed results are expected for Tuesday’s sweep of Chinese data headlined by an expected 4.9 percent year-over-year rate for first-quarter GDP. This would mark slight slowing from 5.2 percent in the first quarter. Monthly data on both industrial production and retail sales are also expected to slow.

The week opens with a busy Monday that will include Japanese machinery orders and Eurozone industrial production and will be highlighted by US retail sales which are expected to once again be solid. UK consumer prices expected to continue to fall in data for Wednesday…Econoday

Just to add one more. I believe it to be irresponsible to simply allow an automated system to run unfiltered by human interaction. Until AI can do your laundry for you unfettered you will absolutely watch $800 losses start to rack up when you turn on your PC over coffee at 4 in the morning lol.

DLRx 103.95

–

with nothing of substance on the econ calendar todahy players have room to argue things out (i.e. consolidate)

the “better qualified” individuals are suggesting ambivalent things about alleged rate cuts with a bottom line attempt at maybe not quiet three cuts as “feasable” this year.

with 10-yr yield nearing 4.5% dlrx is rather subdued in its response.

In his friday yak jerome alluded to details about labor he & gang are watching such as turfing notices and surveys around jobs intentions – two rays of good hope from the FED’s point of view. The CPI numbers that are expected this week appear to be another ray of hope for the FED as “being on the right track” that earlier numbers were but a “bump”

Degenerate traders on the other hand would likely savage rates and ccies on upside surprise releases.

With inflation cooling and economic activity no worse than steady, wait and see is the coming week’s policy directive. Forecasters expect no change at a run of central bank meetings: Reserve Bank of New Zealand and Bank of Canada both on Wednesday, the European Central Bank on Thursday, and the Bank of Korea on Friday. Federal Reserve minutes on Wednesday will detail conditions from three weeks ago when policymakers were cautious in their policy outlook. Data since have not changed the overall picture.

The week’s biggest data release will be US consumer prices on Wednesday which are not expected to show much cooling. If upward price pressure on food prices has abated, energy prices – particularly for gasoline – continued to rise in March. And more important than ever will be service prices that, despite past rate hikes, have continued to be a steady source of upward pressure.

Industrial production from Germany on Monday is not expected to improve, while monthly GDP data from the UK on Friday is expected to be mixed. Chinese inflation pressures in data for Thursday are expected to remain dormant, while Indian inflation data on Friday are expected to remain well above target… Econoday

Of note, EurJpy still holds an overall bid even though we have seen solid sell waves this week so it could stabilize around current levels. Regardless, my preference is the sell side on buy waves.

Morning Bid: Geopolitics, oil and payrolls make for a busy day

A look at the day ahead in U.S. and global markets by Alun John.

It is an unusual start to a first Friday of the month as, with Brent crude oil above $90 a barrel and driving a risk-off tone in markets around the world, investors are not solely thinking about U.S. non-farm payrolls.

Let’s not overstate it. They still are thinking a lot about the always-crucial jobs data, due at 0830 ET (1330 GMT), but after all three main U.S. stock indexes fell by over 1% on Thursday, while Treasuries rallied, it is not the only thing on their minds.

Uptrend is consolidating with the range very clear at 2265-2305 (double top). To shift the risk from the high and suggest a retracement as opposed to consolidation, 2265 would need to be broken.

Viewing gains in EurJpy and Sterling as solid buy side waves against the larger sell side momentum. Hence am short against Yen again in Eur and Usd, while in on the sell side light in GbpUsd but not as confident in that one so observing intently. It appears my preference this week has been the risky venture of counter trading. Noting the yield and hoping it doesn’t decouple with Dxy like it has done more than usual in recent days.

EURUSD

NOW 10766

10757 confirmed will be reached

10760 is the consolidation level; buy below it, sell above it, and tp at it.

10666 confirmed will be reached if it keeps below 10760.

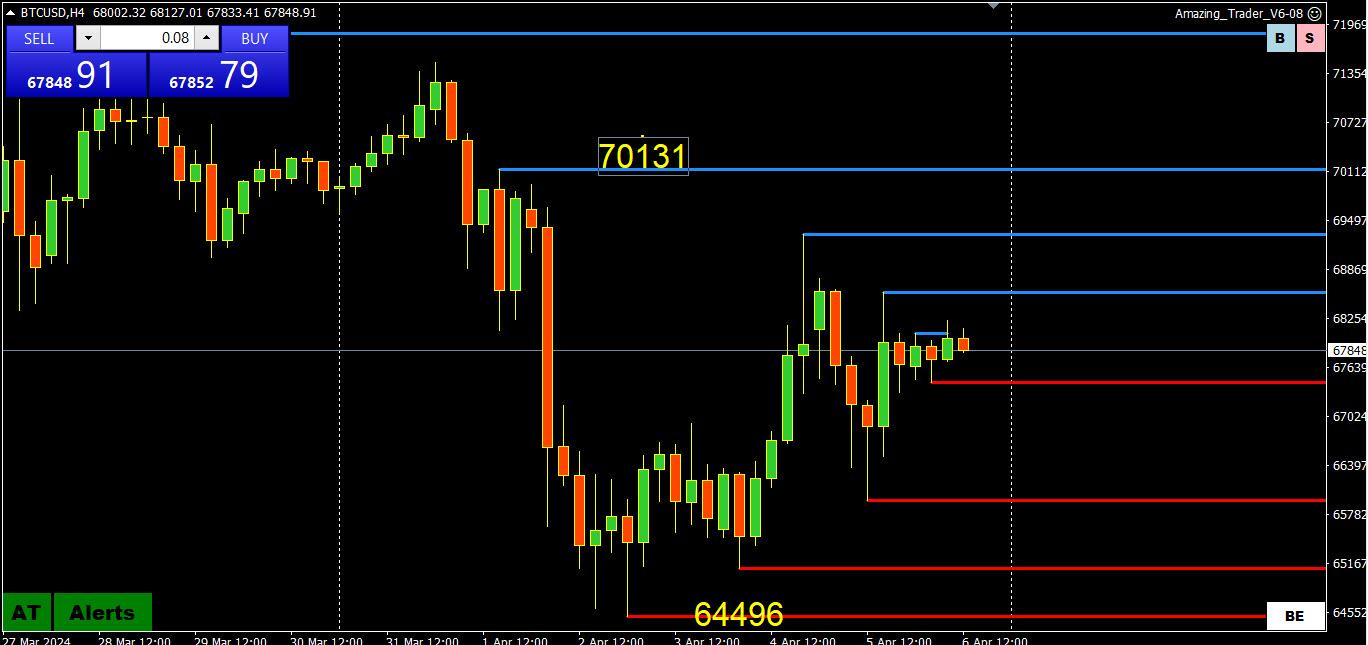

While I don’t trade BTC, I get requests to post a chart.

In this 4 hour chart I have bracketed 65000 — 70000 with moves outside it so far not following through after holding a dip below the bottom end..

Expect choppy trading (an understatement for BTC0 while within this range, next risk )retracement or run at the high) will be dictated by a solid move outside it.

EURUSD

NOW 10766

10757 confirmed will be reached

10760 is the consolidation level; buy below it, sell above it, and tp at it.

10666 confirmed will be reached if it keeps below 10760.

Japan’s quarterly Tankan survey will open the week amid expectations for slowing at large manufacturers. Slowing is expected for US nonfarm payroll growth on Friday to a still strong 200,000 in March from 275,000 in February; wage pressures are also seen slowing but still overheated. Likewise, slowing is expected for Canadian employment on Friday to a very solid 25,000 from February’s 40,700.

Inflation data from Europe will be Tuesday’s and Wednesday’s focus, first from German where some cooling is expected for March then from the Eurozone as a whole where only marginal cooling is the call, to 2.5 from 2.6 percent overall and to 3.0 from 3.1 percent for the narrow core.

Policy news will include the Bank of Canada’s business outlook survey on Monday and minutes from the Reserve Bank of Australia on Tuesday

Evonoday

Author

Search Results

Viewing 20 results - 441 through 460 (of 532 total)